Oil comes centre Stage

Today’s post is about oil, and why it is are the center of markets and the functioning of the world economy. The first few parts will be quite brief as everybody probably already knows the details.

- How did we get to today?

The current business cycle can be traced back to 2018 when Powell began to talk about rate decrease expectations. As interest rate decreases, it spurs people to borrow more and invest more, causing economic growth to come back up.

And of course, the pandemic simply accelerated the process. In addition to unprecedented monetary policy by central banks, global fiscal policy was also unprecedented during the pandemic.

2. Hot economy and inflation:

All of this monetary stimulus led to a super hot economy in the US with very high demand. Increase in demand drove up inflation. In addition, the pandemic fractured supply chains around the world, further exacerbating the problem. As always, when inflation runs rampant, the Fed is forced to raise interest rates.

3. Inflation and Interest rates:

If we pause here and think for a second, why does the Fed HAVE to raise interest rates whenever inflation runs hot? What is this ‘magical’ force that is pushing the Fed to do so? For the answer we have to go back in time to 1971 when Nixon lifted the dollar off the gold standard. The Bretton Woods system which was instituted after WWII pegged the dollar to gold at a fixed exchange rate. This was the beginning of the USD as a global reserve currency. As long as the US promised the fixed dollar/gold exchange rate, the global monetary system would remain intact. However, as the cold war progressed, and the US became increasingly involved in the Vietnam war, and the increased military spending pushed the US into a budget deficit. Even though this was frequently cited as the reason for abandoning the gold standard, another more important reason was the decline in federal revenue:

This meant that the US would eventually have to print USD not backed by gold due to the deepening budget deficit. And sure enough, in 1971 Nixon announced to the world that the USD would no longer be pegged to physical gold.

This was the end of Bretton Woods 1, and the start of Bretton Woods 2. In order to restore faith in the USD as a world reserve currency, the US did three very crucial things which were done by two very important people who helped to shape the world we live in today:

- Volcker. Raised interest rates to combat inflation. But this was only the demand side of the story.

- Kissinger. Went to Saudi to broker a deal with oil. This helped to solve the supply side of the inflation problem, high oil prices.

- Kissinger. Went to China, paved the way for Beijing to enter the UN in 1971 and for Nixon to visit China in 1972. This was the turning point of the cold war. Which eventually led to China opening up in 1978 and the start of the massive globalization push that we see today.

Once American factories got relocated to China, the inflation problem was solved by millions of cheap labor entering the global workforce. Once the Saudi’s agreed to sell oil at USD in exchange for American military equipment, the oil price stabilized and inflation in the US went down dramatically. Once China agreed to open up and co-operate with the US, the soviet union came under immense pressure geopolitically, as Russia’s long border with China suddenly became unsafe. All these in combination helped to lower inflation in the US, and kickstart a second round of economic growth through globalization.

These factors in combination helped to kickstart Bretton Woods 2, which is the world that we live in today. And underpinning the stability of the USD as a reserve currency, is US economic growth and the promise of the Fed to keep inflation in control and maintain the purchasing power the USD. If the Fed loses control of inflation, and we return back to a 1970s scenario, then the world will once again lose faith in the USD a reserve currency. As such, in order to maintain the credibility of the USD, the Fed HAS to combat inflation. Now that we know why the Fed has to combat inflation, let’s take a look at inflation today.

4. Inflation and Oil:

As we can see from this data series, there is a broad correlation between oil prices and inflation. As such, if inflation is to come down, oil prices definitely have to come down. Which brings us to the current relationship diagram below:

Let’s walk through the one by one.

- Energy security and the Ukraine War:

The Ukraine war was a major catalyst driving oil prices up all the way to ~$120 a barrel:

However, do note that even before the war started, oil was trading above $90 a barrel, which is already very high. The Ukraine War and the disruption it had on commodity markets raised a very important question to the entire world: Energy Security. If I am dependent on another country for my energy and raw materials, they can then use it as leverage against me geopolitically. The only way to solve this is to either increase domestic production for countries that can, and to diversify supply sources around the world. However, the problem with diversification is that there are only a few major oil players around the world: US, OPEC/Saudi, Russia, Iran. This was also the reason they the US has historically maintained a strong presence in the middle east, to secure oil supplies. However, things have changed with the advent of shale oil, and the US is now mostly energy self-sufficient. Regardless, the Ukraine war has opened up a can of worms and countries are now forced to rethink energy self sufficiency. Other than oil, perhaps natural gas, coal, or nuclear energy. All of these are difficult long term decisions which will not impact the price of oil in the short term.

- Geopolitics: Iran and Saudi

If the Iranians can once again sell oil on the international market, then global oil prices for sure will come down, helping the US to alleviate inflation pressure. This is also why the US has been working very hard for a Iran Deal 2.0 in recent months.

Saudi: If the Saudi’s agree to dramatically increase oil output, then global oil prices will fall as well. But at this point in time, the Biden administration does not seem to be able or willing to meet the demands of MBS.

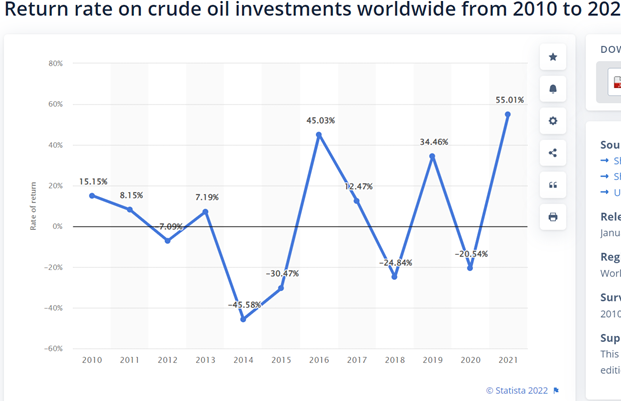

- Climate Change and ESG:

The climate change push and ESG investing mindsets have dramatically reduced the investment in fossil fuels by major banks and energy companies. In addition, if we look at the ROI on oil, it is pretty abysmal.

If we take the average 10 year return, it’s pretty much close to zero. As such, if banks are unwilling to finance long term energy projects due to ESG and low returns, and if countries have been underinvesting in fossil fuels since the paris accord, then it is no wonder why oil prices are high right now because supply is not keeping pace.

In short, the world and the US needs an increase in oil right now to bring down inflation and CPI, and stabilize the economy. The Fed can only bring down demand, but if supply continues to remain tight, prices and CPI can continue to remain elevated for longer than desired. In the short term, what factors can bring down oil prices:

- End of Ukraine war: Unlikely. Because even if the war is over, Russia sanctions will not go away

- Iran Deal: Maybe? 50% probability.

- Saudi hiking oil output: Maybe? 50% probability as well.

As such, oil will definitely stay high in the short term. The best we can hope for is that it steadies around $100/barrel.

In mid to long term:

- Increased oil production by the US

- Increased oil production by Canada

- The big question for markets right now:

The big question for markets right now is, when will oil price come down significantly, and when will inflation as measured by the CPI start to go lower below 4%? If the economy slows down, and inflation and oil prices remain elevated, will the Fed be able to lower interest rates to stimulate economic growth? If it lowers interest rates when inflation is high, this will affect the credibility of the USD as a reserve currency. If it does not lower interest rates when inflation is high and growth is slow, the US economy will most likely be tipped into a recession. Either way, the Fed is boxed in.

As such, the key thing to look out for that will affect short term oil is Saudi and Iran. Can the US get them to increase oil output in the short term?

5. How to invest:

Well, this is the million dollar question isn’t it? The key question to answer is that, what will the Fed do when economy slows down but inflation remains high?

Scenario 1: Iran + Saudi oil come online

Oil prices drop back down, inflation expectations drop back down, real rates rise up, Gold decreases, equities most likely rally a little bit.

Scenario 2: No increased oil production

Oil prices remain elevated, inflation expectations remain elevated, gold slowly decreases over time as inflation slowly subsides, but remains relatively high at around 4%. Equities volatile, unlikely to have a strong rally.

Scenario 3: Iran + Saudi oil say no.

Oil prices move upwards, possibly going past $120 a barrel. Inflation expectations go higher, real rates depressed, gold moves higher, equities very volatile and bearish.

Scenario 2 and 3 will continue to be the main market expectations until long term oil production in the US comes online. And if these scenarios come true, the second question is: What will the Fed do when the economy slows down, but inflation remains high? When will long term US oil production come online? This is the second biggest unknown right now.

Scenario 4: Fed accepts higher inflation rate at 3 – 4%.

In this scenario, gold and equities will rally in a big way.

I think that Scenario 4 is the most likely out of all the different outcomes. But for it to materialize takes time, because at the moment, the Fed is only beginning to raise interest rates and runoff the balance sheet. It has yet to say, “we will accept slightly higher inflation”.

In scenario 4, stagflation is most likely and Ray Dalio did a great talk with Summers on this:

The more I think about scenario 4, and what Dalio said, the more I think that this will materialize. Why? Because as the US continues to re-shore supply chains, this sort of structural change is in itself inflationary. By bringing back manufacturing, inflation will undoubtedly rise up due to rise in wages and rise in cost prices of goods. However, this is not what the market is pricing in at this point in time.

6. What I am doing now:

Thinking deeply about scenario 4, and when is the “buy” opportunity to stock up on gold. From now until May FOMC, it is safe to say one can sit back and enjoy the ride.